“A good person leaves an inheritance for their children’s children…” — Proverbs [13:22]

Introduction

Part I of this series redefined legacy—not as stuff you leave behind, but what you build into your life and family right now. Legacy is about purpose passed on. It’s about living and transferring health, wisdom, wealth, and values in a way that endures.

In Part II of this series, we moved from theory to action: the work of legacy building—intentional effort to raise strong individuals and resilient systems that can carry your values forward.

In Part III, after education and values, after building wealth, after diversifying and acquiring assets, it is not enough to invest in strong assets, but true legacy requires systems to ensure control and stability.

James Kerr of the All Blacks NZ rugby group writes in Legacy, ‘Be a good ancestor. Your legacy isn’t what you achieve—it’s what you pass on.’

What you build must now be protected—not just from markets and taxes, but from time, comfort, and human nature.

📜 1. Establish Family Governance

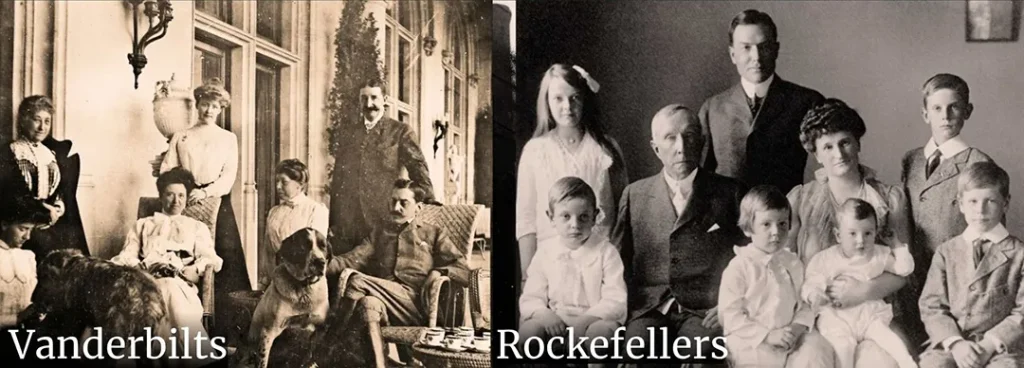

Two great families, about one hundred years ago, were the wealthiest in America.

One is wealthier than ever, the other’s fortune is gone.

Trusts & Estate planning were critical, but real estate also played a role

The Vanderbilts once owned ten mansions on Fifth Avenue alone.

The Rockefellers invested in income producing assets, including rental real estate.

*they had mansions too, but they understood the difference between an asset and a liability.

“Discipline equals freedom.” – Jocko Willink

Family governance is how values survive when the founder is no longer in the room.

- Governance ≠ control

- Governance = shared clarity + aligned decision-making

- Avoiding governance is how families drift apart

The Rockefeller family established a formal family constitution to provide a framework for managing their wealth and preserving their family legacy across generations. This constitution outlines the family’s shared values and principles, such as stewardship, philanthropy, and the importance of financial literacy, influencing their estate planning and trust governance to ensure wealth preservation and a unified purpose.

The family constitution forms the basis for estate planning documents and the governance of family trusts, ensuring aligned financial values and controlled allocation of funds.

- Create a Family Mission Statement that defines what your family stands for.

- Consider a family council or board if you have shared assets, businesses, or philanthropic plans.

- Schedule regular family meetings to discuss finances, roles, and vision, so everyone stays aligned.

This doesn’t require billions and doesn’t have to be complicated

A family constitution can be:

- 1–2 pages

- Values + rules + rhythm

- Reviewed annually

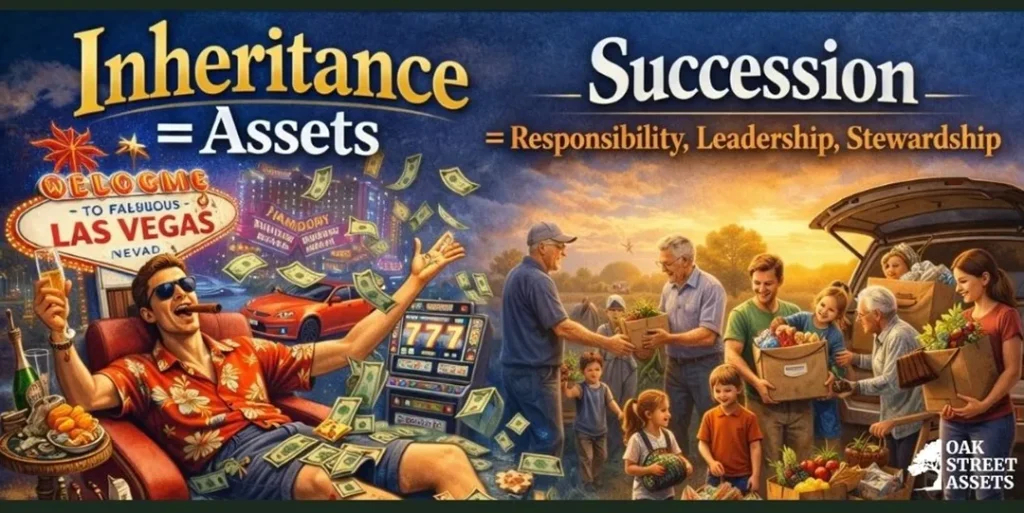

Remember Sudden Wealth Syndrome.

What happens when individuals receive a large amount of money quickly such as professional athletes, lottery winners, inheritances without the skills, systems, identity, or governance structures to manage it?

The result is often overspending, poor investment decisions, breakdown of relationships, and ultimately loss of the wealth.

Shirtsleeves to shirtsleeves in three generations.. or the Lottery Curse.

Sudden wealth without systems doesn’t create freedom. It exposes weakness.

🎓 2. Plan for Leadership and Mentorship

- Identify who can lead—not just who inherits, but who has the character and competence to carry on your legacy.

- Mentor them personally, or line up trusted advisors who can help guide them.

- Teach them to handle conflict, make decisions, and communicate clearly—skills essential for sustaining family unity.

If you could only leave one thing to your children, would it be your stuff or your wisdom?

🔩 3. Revisit, Review, and Reinforce

Life changes, and so should your plan. Certainly one should update estate and legacy documents after major life events (births, deaths, marriages, divorces).

More importantly, it is recommended to review and reassess your family mission and governance regularly—new perspectives may strengthen your vision and such a practice will allow for regular reassessments after major life events.

- Annual legacy review

- Life-event triggers

- Generational handoffs

Once values, governance, and leadership are clear, structure can now serve them.

Financial Infrastructure

Structures, trusts, and family systems that endure are the second half of the family constitution.

Build Financial Infrastructure

This is where traditional estate planning intersects with true legacy planning.

- Use trusts, entities, and insurance to protect assets

- Ensure your will and medical directives are in place

- Organize your records so your heirs aren’t lost

- Create giving plans to pass on generosity

But don’t stop there. Teach the next generation how to manage these assets wisely. Don’t just build wealth—build wisdom (more on this in the final installment of Legacy by Design).

I often recommend What Would the Rockefellers Do? by Garrett Gunderson—not as a biography, but a short study of legacy systems. Rather than focusing on individual wealth or stock picking, the book reframes wealth as a responsibility to be stewarded, showing how the Rockefellers built enduring family wealth through operating businesses, cash-flowing assets, thoughtful use of debt, trusts, education, and intentional governance. These structures are designed not just to grow capital, but to preserve values, purpose, and capability across generations.

Make Giving a Family Affair

Generosity is a core value for successful families and cultures with good reason and shared giving from an early age helps them understand their identity and prevents entitlement. It creates an abundance mindset and trains stewardship.

- Develop a charitable giving strategy together—let children or grandchildren help choose causes.

- Use vehicles like donor-advised funds, family foundations, or charitable trusts to formalize giving plans.

- Reflect on why you give—the motivations behind your generosity matter as much as the gifts themselves.

🚚 You never see a U-Haul behind a hearse.

Inheritance Plans: Models, Tradeoffs, and Intentionality

Over the years, I’ve seen a wide range of inheritance models. Some are thoughtful and effective. Others are well-intentioned but quietly destructive.

While the full spectrum of inheritance strategies is beyond the scope of this article, it’s important to understand that how you pass on assets matters just as much as what you pass on. There is no one-size-fits-all solution, only intentional tradeoffs.

Below are several common inheritance approaches, each with strengths and risks. These models will be explored in greater depth in a future article.

Common Inheritance Models

- Traditional Trust Structures

- Distributions released at specific ages (e.g., 25/30/35)

- Often combined with incentives for education, employment, or stewardship

- Useful, but insufficient without preparation and values

- All Assets Transferred at Death

- Simple and decisive

- High risk of overwhelm, entitlement, or mismanagement if heirs are unprepared

- “On Your Own at 18”

- Emphasizes independence (I’ve seen this go both ways)

- Often confuses abandonment with strength and can fracture relationships

- Conditional or Challenge-Based Models

- Brewster’s Millions–style requirements (I know a guy doing this)

- Encourages capability, but must be aligned with values, not gimmicks

- Public Examples

- Shaquille O’Neal: “Two degrees to touch Daddy’s cheese.”

- Education-Only Inheritance

- Focuses on funding education and development rather than lifestyle

- Effective when paired with identity and responsibility training

Each of these models answers a different question:

Are you trying to create comfort or capability?

The right inheritance plan depends on your values, your family dynamics, and the preparation you’ve done along the way. Inheritance should never be the first legacy decision you make—it should be one of the last, built on top of identity, character, and stewardship.

Assets transferred without preparation often become liabilities.

In a future article, we’ll explore these inheritance models in depth, including how families blend multiple approaches to align wealth transfer with long-term legacy.

Create a Team – Family Offices

If your net worth is large enough ($20M-$50M), people often create a team of professionals that help support the family called a Family Office. This is often out of necessity as proper oversight and diversification requires more experience and attention. There are also ‘multi-family offices’ that are shared among multiple families that may not require full-time assitance.

NOTE: you do not have to be super wealthy to benefit from the philosophy and structures underlying a family office. Governance, coordination, and values alignment scale down well.

A family office is a private organization set up to manage the wealth, investments, and affairs of a wealthy family. Instead of the family juggling financial advisors, accountants, lawyers, and business managers separately, a family office brings these functions under one umbrella so the family can focus on their lives, values, and long-term vision.

What they do:

- Wealth Management: Investing, portfolio allocation, risk management.

- Financial Planning: Tax strategy, estate planning, trust structuring.

- Administration: Bill pay, accounting, payroll, reporting.

- Philanthropy: Managing charitable foundations, legacy planning.

- Lifestyle Services: Concierge support, family governance, succession planning, even travel arrangements.

At its core, a family office isn’t just about growing wealth—it’s about protecting it across generations and aligning financial decisions with the family’s values, goals, and legacy.

💡 Life’s work is meant to be shared, not stored.

Conclusion

Legacy isn’t created in a moment. It’s shaped through years of intentional modeling, teaching, investing, and connecting. While creating a legacy for generations is a worthy goal, remember to be present and live thoroughly now and accumulate those ‘memory dividends’!

In Part IV, we’ll complete this Legacy series sharing the practices and support systems that ensure your legacy is preserved over time: how to walk the path and live the legacy.

Until then, remember: Legacy may not start with documents, but it continues through intentional systems!

Reminder: Do not delay living for the sake of leaving.

What’s Next: Implementing Practices and Refining

This series hopes to guide you through designing, building, protecting, and living your legacy:

Part I: Redefining Legacy – It’s not about net-worth

Part II: Building the Legacy – Creating assets of health, wealth, and wisdom

Part III: Protecting the Legacy – Structures, trusts, and family systems that endure

Part IV: Living the Legacy – Daily practices, coaching, and modeling that keep your legacy alive

Reach out to learn about the systems, affiliates and resources we are using to create our legacy.